If you have purchased a caravan, motorhome, or any other type of RV, you will understand its value. Not only in dollar terms, but also in the pleasure it can bring you as you embark on your camping trip or your first trip around Australia.

It doesn’t matter if your rig only cost a few thousand dollars or up to $200,000. The loss of it would bring a significant financial burden. Including the disappointment of not being able to continue your trip.

It is imperative therefore that when you purchase your RV, you get the right insurance cover. Having spoken to many other RV owners over the last five years, we have found that the old Castrol adage, “Oils ain’t Oils”, can also be relevant when talking insurance cover:- “Insurance ain’t just Insurance.”

With a multitude of insurance companies out there to choose from, how do you go about choosing the right one?

Whilst preparing for our big trip, we spent quite a bit of time researching different types of RV insurance. During the course of the research, we heard several horror stories about other travellers’ experiences. Some after having chosen either the wrong type of policy. Or a disreputable company misleading or misrepresenting their policy. Others simply misunderstanding what they were and were not covered for, with the result being that they were left without valid, appropriate cover.

Do you have more than just an accident cover?

Unlike car insurance, your RV is different. It is not just traffic accidents or theft you need to consider. You live in your RV, in some cases full time. Therefore if something were to happen, you need to make sure you are adequately covered for all relevant scenarios.

For e.g., if you did lose your RV in an accident, where would you stay and how would you get home? What if your awning blows off? Are you covered for floods? Believe me, having been caught in this exact situation, it was a relief to know that we were in fact covered for this.

Our Motorhome is trapped in rising flood waters.

As you are living in the RV, covering your contents is another important factor you should consider in your selection process. In some cases, where you have your own home and contents insurance, some cover for personal items may be included when you travel away from the home, but this is not always the case. If you are a full time traveller, which many of us are, and do not have a permanent place of residence, you may not be covered for this.

It is important therefore to make sure not only that the insurance policy you select will fully cover your needs. Also that the insurance company standing behind the product is reputable and will be there for you when you need it most.

Unfortunately, most people find this out when it is too late. It is not until they have an incident and need to make a claim that they find out what is in the fine print of an insurance policy.

Whilst there are many generalised insurance policies in the market, there are very few specialised insurance policies for RV’s. Some have just the basic cover with none of the bells and whistles. I realise now that had I taken one of those policies, I would have been out of pocket by thousands.

RV insurance policies will vary in price from a few hundred dollars to over $1000. Reflecting what they include or, conversely, what they do not include in the policy. While some will save you a few dollars at the time, you may find it will cost you more in the long run. For us personally, making sure we found the right policy has proved invaluable.

Do you have a fusion cover?

One such example for us was when we made a claim for the replacement of our fridge. When I started looking at the basic policies, I noticed some did not cover fusion damage. I questioned myself as to whether we would need it. In the end, I found a policy that included it. Yes, I paid a bit more, but it paid for itself when, two years later, we lost our fridge due to the motor burning out. I was not only able to replace the fridge, but also the food that was spoilt along with it.

Another such incident for us was when we were trapped in rising floodwater. We were airlifted out and left without our home for quite some time. It was comforting to know that we were covered not only for the damage to be repaired, but also for the recovery of the Motorhome, temporary accommodation, and our contents were also replaced.

Do you have contents cover?

There are many stories such as ours. The point I am trying to make here is to make sure you research thoroughly before you purchase any RV Insurance policy. Also, find out what cover is included in that policy. I would urge you to take the time and get your hands on as much information as you can. Ask for the PDS in all cases and when you have it, make sure you actually read and understand it. If you are unsure about some part of it, contact the insurer and ask them. By law, the insurance company must disclose everything they do and do not over.

To assist you further, I have outlined below some very basic terms insurance companies use. Some that you may also like to consider when making your decision.

BASIC TERMS

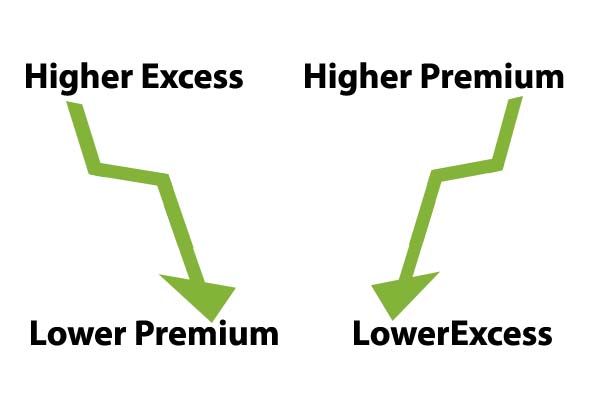

Excess

What is it and why do they have it?

Excess is the term that is used for the amount of money you have to pay when you make a claim. This may vary with different insurers and policies. If an insurer offers varying levels of excess, this will usually affect the amount of the overall premium. A lower excess will increase the premium, whereas if you are prepared to pay a higher excess, it will often reduce the annual premium.

Excess is essentially put in place by insurance providers in order to manage the number of claims they receive. It prevents constant small claims being made by policyholders. In theory should mean that because the insurance company receives less claims, the better for them. So technically, premiums should be lower overall.

In deciding which level of excess best meets your needs, it is worth considering what level of loss you would intend to make a claim for. In other words, are you planning on claiming only in the event of a total loss. E.g. your RV is stolen or totally destroyed in a major incident. Would you like to cover for minor incidents as well, such as minimal panel damage from a storm or accident, flood damage, or for loss of contents?

Knowing this in advance can assist you in determining the level of excess you wish to pay, and if it is worthwhile.

At Fault

Also, common terms are at fault or not at fault which you should be aware of. Terms that are closely connected to your excess and when you will need to pay it.

At Fault, as it suggests, is for times where you are responsible for the damage sustained to your RV. E.g. if you were involved in a motor vehicle accident and it was as a result of your driving. Then you may be deemed to be at fault. Be asked to pay the excess at the time of making a claim.

If, however, it is evident that you were not the cause of the incident. You are able to obtain the name and contact details of the responsible party. Then you may be deemed to be not at fault. An example is when your RV is parked in a campground and someone else’s caravan accidentally rolls into it.

If you are deemed not at fault and the responsible party can be identified, your insurance company may not ask you to pay the excess. Instead, they will take this up with the other party or their insurance company.

You should also note that any No Claim Bonus you are eligible for may be affected should you have to make a claim. With many variables to consider when it comes to who is at fault and who is not, the installation of a dash cam can provide valuable evidence for some situations.

Agreed Value or Market Value

It is important that you know in advance how much your insurance will cover you for. It is especially if you are in a total loss situation. Some insurers will offer the choice of either Market Value or Agreed Value. Some will only offer one or the other.

Market Value – This means that in the event of a total loss, they will pay you the current value your RV would fetch on the market. Not necessarily the amount you paid for the RV or what it would cost you to replace it. To establish this value, often a combination of an assessor’s appraisal and valuation guides are used. This form of cover may lead to a cheaper premium but can sometimes lead to disappointment to the owners when they and the insurer may not agree on the market value at the time.

RVs depreciate over time. Even if you paid $50,000 to purchase your van, you may find that in 18 months’ time your insurance company may think it is only worth $30,000. Wherein your eyes its value still holds much closer to the $50,000 you paid for it.

Agreed

Agreed Value – means that you and your insurer will determine the value of your RV at the start date of the insurance policy. Both will agree that this remains the maximum value that can be paid out in the event of a total loss during the period of the policy, usually 1 year. The value may be worked out by a variety of methods. Including the amount the RV was purchased for, and once again, assessor and valuation guide input. However, you have the peace of mind of knowing that if you were to suffer a total loss, you would know in advance the amount you were likely to get back.

Many insurers also offer a total replacement value within the first two years of your ownership of a new RV. This means that no matter what the market value of the RV at the time of the claim, if it were deemed a total loss, the insurer would replace the RV with the same model, or as close as possible to it. Regardless of the cost of the new one, allowing for any price increases that may have occurred.

Questions to Ask

In general, there are two essential questions you should ask any prospective insurer:

- What am I covered for?

- What is NOT included in the policy?

Whilst many are happy to mention the inclusions, it is sometimes what is not included that can make the difference.

Other questions you may consider asking are:

* If you are on a trip, become ill, and need to get back home urgently, how would you do so? How would you manage? Is this covered?

* If this cover is provided to get you back home, would it include everyone in your travelling party or just the driver? Would it also include the RV?

* If your solar panels or generator were, say, 10 metres away from your RV and not under your awning, would they still be covered?

* How much automatic cover do you have on your contents, or are they covered at all?

* Are you covered for towing in the event of a mechanical breakdown, as well as after accident or theft damage? What if your motorhome has engine problems or the axle falls off the caravan? Is any towing covered?

* What if you lose your keys or the locks are damaged? Is this covered?

* Does the policy include free windscreen replacement each year?

* If your RV is stolen or in an accident, is a replacement vehicle provided, and if so for how long?

* If you tow a trailer, is it covered?

* Are you permitted to conduct emergency repairs to get you on your way and up to what value?

This list is not exhaustive and you should not only ask these questions. Also if the type of cover you require is provided, be sure to take into consideration any dollar value or time limits placed on that cover.

Note from the Author – Rob Catania

Please bear in mind that this article is written from my point of view. I am not an insurance expert, nor do I profess to be. It is based on my own experiences and research. It is intended as a guide only. Prior to purchasing any insurance policy, I would encourage you to make your own enquiries. Obtain a full PDS statement, and make sure you pick the best policy to suit your budget and your needs.